We are delighted to be hosting a blog post from Dr Aisha Al-Sarihi, who is currently a visiting scholar at the Arab Gulf States Institute in Washington. Having recently earned her PhD at Imperial College London investigating the challenges and opportunities for adopting renewable energy in Oman she has sent us a really interesting blog on the impacts of carbon pricing on some of the oil-rich countries around the Persian Gulf.

The Arab Gulf States – Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE –are highly vulnerable to oil price shocks due to their high economic reliance on oil and gas export revenues. Historically, oil price shocks have been a source of pressure on the Arab Gulf States economies. However, only since mid-2014 have oil prices seemed to pressure on political regimes to consider domestic economic reforms and development of alternative sources of income (i.e. economic diversification). Among other measures, energy subsidy reforms, privatization, and even a value added tax have been discussed and introduced.

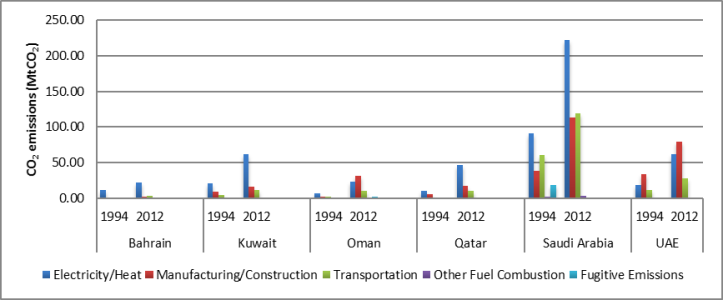

In the Arab Gulf States, economic diversification does not necessarily mean a transition to low-carbon economy. Recent economic diversification efforts have been increasingly directed towards developing downstream energy-intensive industries such as petrochemical industries which are 100% reliant on oil and gas for their operation. In fact, the Arab Gulf States are by far the world’s biggest emitters of climate changing greenhouse gas emissions (GHG) on a per capita basis. Climate-related emissions are rapidly increasing in the Arab Gulf States. GHG emissions increased on average 6% annually between 1970 and 2012 in parallel with increases in GDP and energy consumption. According to the World Resources Institute, the industrial and power sectors are the major CO2 emitters in the Arab Gulf States, followed by transportation (Figure 1).

To avoid long-term negative implications – such as increasing total CO2 emissions and deterioration of air quality associated with increasing downstream petrochemical energy intensive industries, fossil fuel subsidy reforms, enhancing energy efficiency and the use of clean energy technologies are indeed instrumental to tackle such issues. In this article, carbon pricing is proposed as a useful instrument to complement the aforementioned tools.

Carbon pricing means putting an explicit price on carbon pollution as a means of bringing down emissions and drive investments into cleaner options. A carbon price gives an economic signal for the polluters to decide for themselves whether to discontinue their polluting activity, reduce emissions, or continue polluting and pay for it. Already, over 40 countries have a price on carbon pollution.

The most popular carbon pricing approaches are: emissions trading systems (ETS) and carbon taxes. An ETS, called a cap-and-trade system, pre-defines the total amount of emissions to be reduced (the cap) and allows those industries with low emissions to sell their extra allowances to larger emitters. In this way, supply and demand for emissions is created, based on which the market price for GHG emissions is established. A carbon tax, on the other hand, directly sets a price on carbon by defining a tax rate on GHG emissions – or more commonly – on the carbon content of fossil fuels, i.e. a price per tCO2e. It differs from ETS in that the total amount of emissions that need to be reduced are not pre-defined.

Carbon tax scheme is the best method to fit the national and economic circumstances of the Gulf States in the short-term as it aligns with recently introduced value added tax schemes. This could possibly minimize the administration costs. Also, unlike an ETS scheme, a pre-defined carbon price mitigates volatility to price fluctuations associated with flexible carbon prices. However, while a carbon tax guarantees the carbon price in the economic system, it does not provide certainty about the environmental impacts. Accordingly, given the expansion of the downstream energy intensive industries in the Arab Gulf States, an ETS scheme (i.e. capping the total emissions) can be adopted in the medium- to long-term basis to ensure that the Gulf States are not becoming major contributors to global climate change.

But how much revenues can be raised from imposing price on carbon emissions in the Arab Gulf States?

Professor Lord Nicholas Stern warns that current carbon pricing is too weak to achieve goals of the Paris Climate Agreement. In a speech at the One Planet Summit on 12 December 2017, he warned that “to deliver the goals of the Paris Agreement prices must reach $40-80 per tonne of carbon dioxide by 2020, and $50-100 by 2030.”. To give an indication of how much annual revenue can be raised in the Arab Gulf States, four carbon pricing scenarios, as suggested by Professor Stern (i.e. $40, $50, $80 and $100), are imposed to total CO2 emissions produced in 2014 (Table 1). Surprisingly, in some cases, total revenues that can be raised from imposing a price on carbon exceed the total amount of subsidy allocated to the fossil fuel sectors. For instance, in Oman, the estimated total revenues from carbon pricing under the $40 scenario equals to USD 2,446,760,000 (around USD 2.4 trillion) was three times higher than the total amount of subsidy allocated to power sector in 2014 (USD 745,790,000 or USD 0.7 trillion). Under the $40 scenario, the carbon price revenues in the UAE are also almost three times higher than the total estimated revenues from value added tax (i.e., $3.3 bn). To-date, none of the Arab Gulf States impose a price on carbon emissions.

| Country | CO2 emissions* | Annual revenues (in USD) from carbon pricing per scenario | |||

|---|---|---|---|---|---|

| Scenario Assumption | $40 per ton | $50 per ton | $80 per ton | $100 per ton | |

| Bahrain | 31,388 | 1,253,520,000 | 1,566,900,000 | 2,507,040,000 | 3,133,800,000 |

| Kuwait | 95,408 | 3,816,320,000 | 4,770,400,000 | 7,632,640,000 | 9,540,800,000 |

| Oman | 61,169 | 2,446,760,000 | 3,058,450,000 | 4,893,520,000 | 6,116,900,000 |

| Qatar | 107,854 | 24,041,880,000 | 30,052,000,000 | 48,084,000,000 | 60,105,000,000 |

| Saudi Arabia | 601,047 | 24,041,880,000 | 30,052,000,000 | 48,084,000,000 | 60,105,000,000 |

| UAE | 211,370 | 8,454,800,000 | 10,569,000,000 | 16,910,000,000 | 21,137,000,000 |

The revenues raised by carbon pricing can be used as a new source of income which can be distributed directly back to the population. Another option is to direct revenues raised from carbon pricing towards clean energy research and technologies. This will enable Gulf States to diversify their economies in the long term, at the same time as fossil fuels are being phased out in order to stabilize the world’s emissions. Carbon pricing is an opportunity for the Gulf States to pursue a transition to low-carbon economy as well as an opportunity to meeting the requirements of Paris Climate Agreement. Given the Gulf states are in many ways among the most vulnerable to the effects of climate change including increased average temperatures, less – or more erratic – precipitation, and sea level rise in a region which already suffers from aridity, recurrent drought and water scarcity, urgent action to transition from fossil fuel dependence to clean energy is useful for the region to both meet the Paris Agreement emissions reduction goals and hence reduce the adverse climate impacts on the region.

Finally, it is vital to get the carbon prices right in order to achieve effective results. Gulf States should pay attention to the negative carbon price. In other words, it is important to eliminate the gap between carbon prices and fossil fuel subsidy so that fossil fuel subsidies do not act as an incentive in the opposite direction to carbon prices – incentivizing fossil fuel-dependence.

Acknowledgement

Thanks to Dr Helena Wright for commenting on the first draft of this blog.

Biography

Dr Aisha Al-Sarihi is currently a visiting scholar at the Arab Gulf States Institute in Washington looking at the potential for climate policy integrity with economic diversification strategies in Saudi Arabia. Her research interests include energy, climate, and renewable energy policies and political economy with a focus on the Gulf Arab states.

She holds an MSc and BSc in environmental science from Sultan Qaboos University and a PhD from the Centre for Environmental Policy at Imperial College London. Her thesis was focused on studying the challenges and opportunities for adopting renewable energy in Oman.

While finishing her PhD she worked on the LSE Kuwait Programme, researching the incorporation of climate change policies into the Gulf Cooperation Council‘s economic diversification strategies. Before moving to Washington, she was involved in an Oman-based project to provide expertise on possible environmental policies for the country’s future energy-mix.

[…] Al-Sarihi via Energy Futures Lab Oct 24, 2018 Mountains in Oman (Tristan […]

LikeLiked by 1 person

Reblogged this on aishaalsarihi.

LikeLike